Navigating to the Refi Risk of Waiting Report

You can find your Affordability Calculator within Client Manager and within the Calculator tab of the left-hand navigation menu.

Navigating through the Client Manager

Client Manager allows you to create reports for your clients using previously saved loan and property details, saving you time when building new scenarios.

Navigating through the left-hand sidebar menu

To access the Affordability Calculator using the left-hand sidebar menu, click Calculators, then click Risk of Waiting.

💡 Helpful Tip: You can favorite the Refi Risk of Waiting Calculator by clicking the star next to its name, so it's easier to find next time.

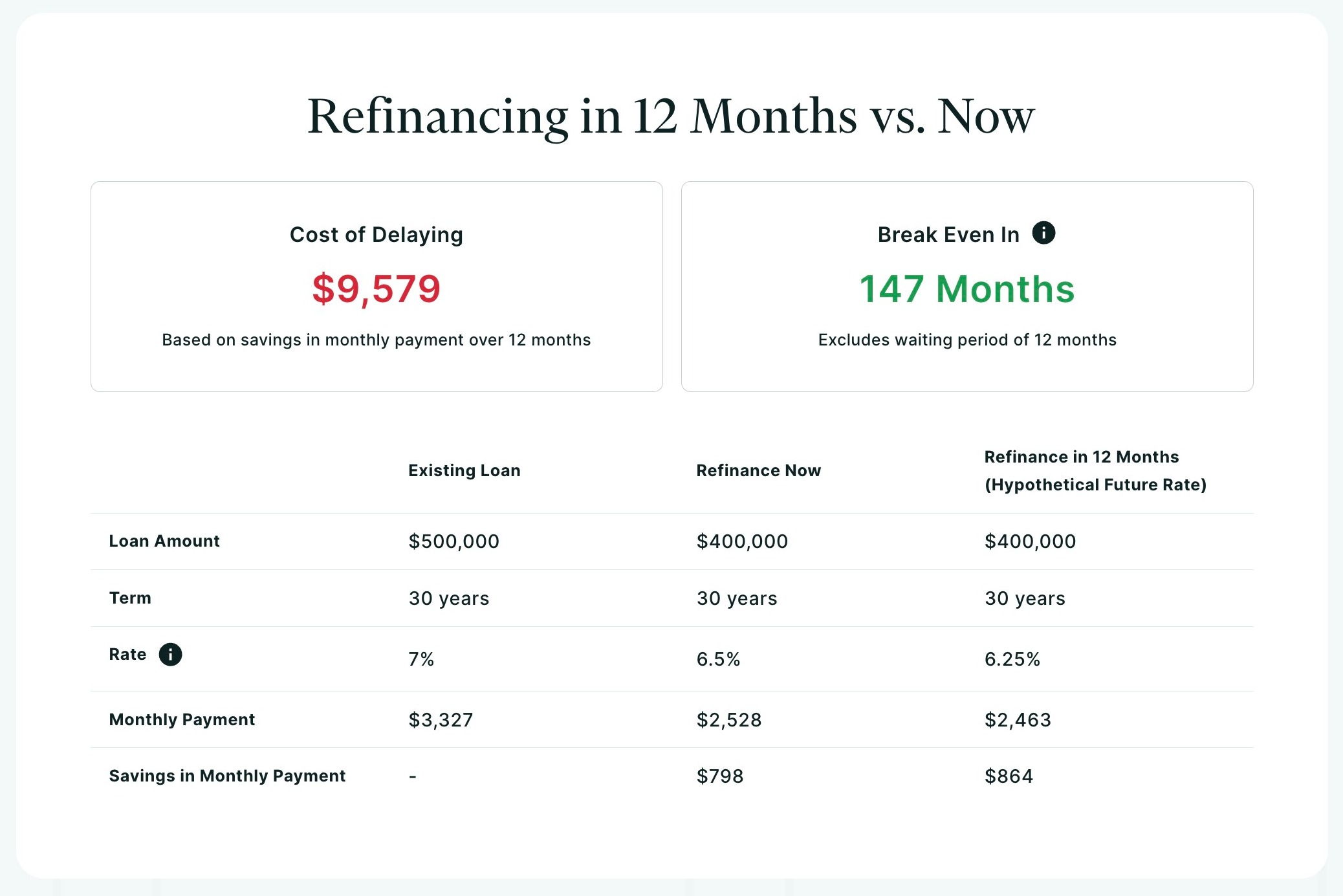

Understanding Your Results

In the results, you will find two key metrics:

-

Cost of Delaying: This shows how much your client could lose by delaying the refinance of their home for a hypothetical future rate. See below for how we calculate cost of delaying:

- Cost of Delaying = (Existing Payment - Refinance Now Payment) * Months Waiting

-

Break-Even Period: This metric tells you how many months it would take for the savings from refinancing to cover the initial costs. In the example, refinancing now breaks even in 77 months, excluding the waiting period of 12 months. See below for how we calculate the break-even period:

- Break Even Months = Savings Lost By Delaying / (Refinance Now Payment - Refinance in X months)

In the table, you will find three different loan scenarios:

- Existing Loan Scenario: Breakdown of monthly cost if your client were to remain with the same loan and not refinance at all.

- Refinance Now: Shows the monthly savings your client will receive by refinancing today.

- Refinance in 12 Months (Hypothetical Future Rate): Shows the savings your client would receive if they wait for their hypothetical rate in a certain number of months.

With this summary, you will be able to show your clients not just the monthly savings they can receive by refinancing now versus in the future, but also how long they would need to wait to recuperate the cost of waiting for a hypothetical rate, vs the real savings they can achieve now. In addition, if monthly cash flow is important to your client, the immediate savings they would receive from refinancing may be a greater priority than waiting for a potential rate in the future.

Need Help?

Have questions? Click here to submit a support ticket.