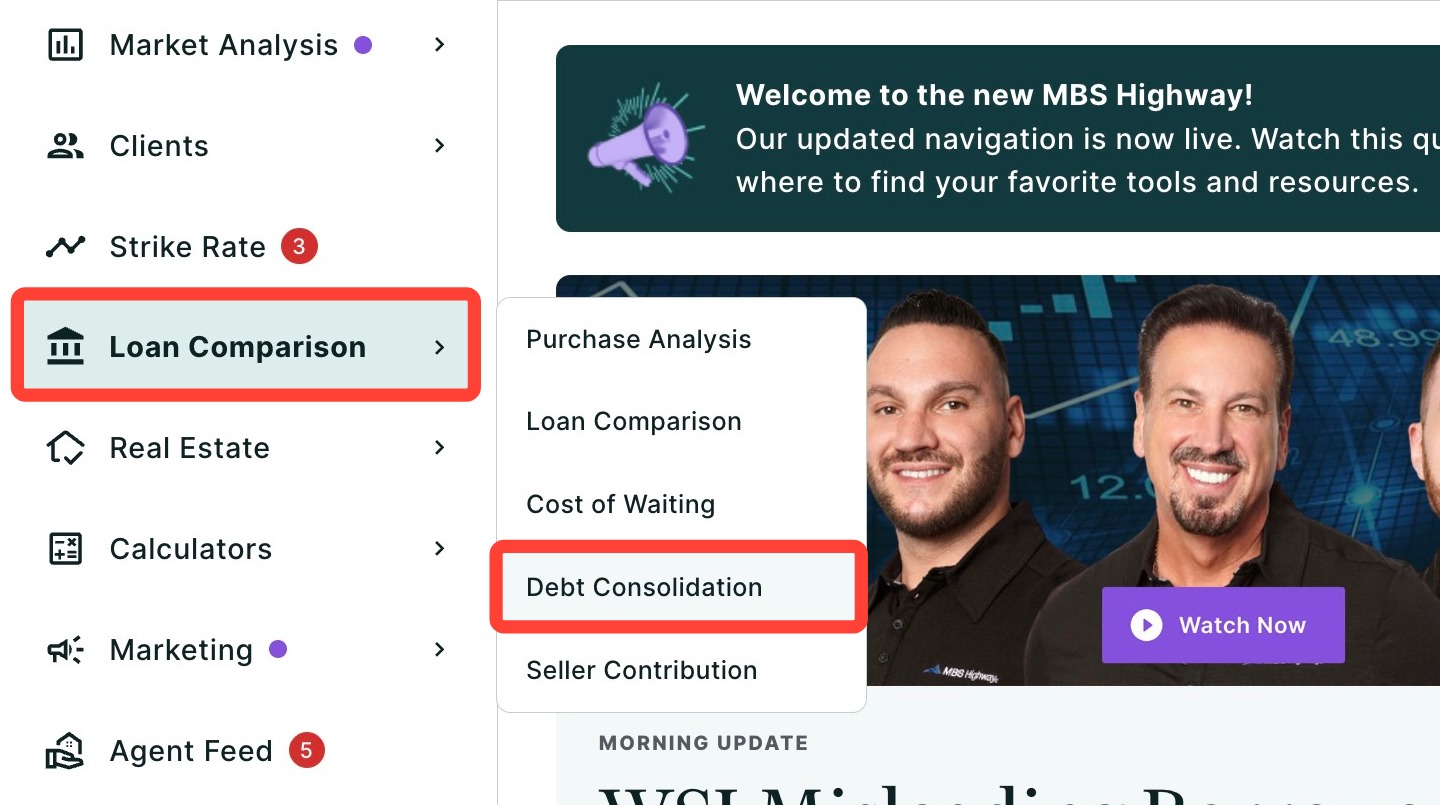

Navigating to the Debt Consolidation Report

You can find your Debt Consolidation Report within Client Manager as well as within the Loan Comparison sidebar menu.

Navigating through the Client Manager

Client Manager allows you to create reports for your clients using previously saved loan and property details, saving you time when building new scenarios. To learn more, click here.

Navigating through the Menu

To access the Debt Consolidation report using the left-hand sidebar menu, click Loan Comparison, then click Debt Consolidation. By default, the Refinance report will be displayed.

Helpful Tip: You can also search and favorite reports, tools, and calculators. Click here to learn how.

Front and Back Ratios

At the top of the report, you’ll see the front and back ratios, the max for both, and the dollar amount by which the new monthly payment is under or over these thresholds.

- The front ratio is calculated by dividing housing expenses by the borrower's gross monthly income.

- The back ratio is calculated by dividing the total monthly debt payments by the borrower's gross monthly income.

Available Cash In-Hand and Applicable Debts

Next, you will see the Available Cash In-hand which will help your client determine which debts they would like to pay off using the new proposed loan.

- Click on the checkboxes next to their corresponding debts to include them in the loan refinance.

- The subtotal of included debts, cash in-hand, and total cash out will automatically be updated below as you add and remove debts. Your customers' monthly deficit or savings will be listed below.

- You also have an option to reduce the loan amount, changing the available cash in hand. To edit the available cash in-hand amount:

- Click Edit Amount.

- Enter the amount you would like the loan amount reduced by.

- Click the checkbox.

Savings Summary

In the next section, you will find a summary of savings in dollars, time, and payments.

- If your client now has monthly savings with their debts consolidated, the monthly dollar amount will show in green under the Savings section.

- The tool shows what it would look like if they applied these savings towards their principal payment every month (click Edit to change the amount of Savings Applied Towards the Principal).

- You will also find the amount of time and number of payments saved under the Term and Payment sections.

- You can use toggle seen below to hide this section.

Existing vs Proposed Loan Scenarios

In the next table, you will see a comparison of the Existing and Proposed scenarios.

- At the top of the table, you'll see the mortgage balance for both scenarios, as well as their respective unconsolidated debts.

- The next three sections provide a side-by-side comparison, highlighting the savings achieved through debt consolidation. You can modify the year displayed for the first two rows by using the drop-downs shown in the image above. Please note that the last row, which represents the end of the term, cannot have its year edited.

Total Savings

Next, you will find the total savings in dollars and years by your client consolidating their debt along with an explanation of how we calculate that savings.

- Please note: these calculations assume that the minimum payment is being made on the revolving balance(s) without additional payments towards the principal.

Payments

This section shows a comparison between the borrower's current total payments and the proposed total payments after debt consolidation.

Loan Details

Lastly, you will find a comparison of debts, equity, and loan details between the existing and proposed scenarios.

Need Help?

Have questions or want to learn more? Submit a ticket or call us today!